Welcome to Carloancalculator.com.au.

You can use our car loan calculators to understand your estimated repayments when you take out a car loan. Our calculators and website resources are here to help you understand all aspects of car loans and choose the loan that’s best for you. Learn about the different types of loans, what to look for and how to apply with Carloancalculator.com.au.

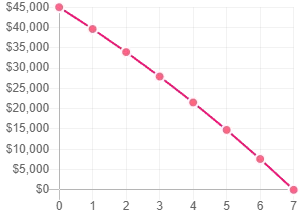

Your estimated repayments are

Car Loan Calculator Assumptions

The figures provided should be used as an estimate only, should not be relied on as true indication of your car loan repayments, or a quote or indication of pre-qualification for any car loan product. The figures are based upon the information you put into the calculator. We have made a number of assumptions when producing the calculations including:

Loan term, vehicle purchase price, and loan amount:

We assume the loan term, vehicle purchase price, and loan amount are what you enter into the calculator.

Interest rates: We assume that the rate you enter, is the rate that will apply to your loan for the full loan term.

Interest and repayments: The displayed total interest payable is the interest for the loan term, calculated on the entered interest rate.

Payable over 3/4/5 years figure excludes any balloon payment

Explore by Make

*Comparison rates based on a loan of $30,000 for a five-year loan term. Warning: this comparison rate is true only for this example and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. Rates correct as of 11 April 2024.

How does the calculator work?

To use this calculator, you will need to:

Enter your preferred interest rate:

Lenders are required to show two types of interest rates when advertising their product - the advertised rate and the comparison rate. The advertised rate is simply the interest rate of the loan, whereas the comparison rate shows the true cost of the loan as it includes all costs and fees.

Select a loan term:

A loan term refers to how long you have to pay off the loan. Typically, car loans in Australia have a term of 1-7 years. A shorter term means you will have a higher monthly repayment but less overall costs, while a longer term means a lower monthly repayment but the total interest charged is higher.

Balloon payment:

A balloon payment is a one-off lump sum that you agree to pay your lender at the end of your car loan term. As balloon payments will generally be a large portion of your loan, for example 30% of your loan balance, they can reduce your ongoing loan repayments and help save you interest over the life of your loan.

View results:

Once you have entered all details, you can view your approximate car loan repayment. You can change your preferences and view your car loan repayment as a monthly, fortnightly, or weekly figure.

New, used and business car loans

There are many different types of car loans available in the market. The popular ones are new, used, and business car loans.

New

New car loans refer to new or sometimes demo used vehicles, generally less than 2 years old.

Used

Used car loans refer to vehicle financing of secondhand cars typically up to 12 years of age.

Business

This is a type of finance that specifically covers cars used for business, commercial enterprises and employees. There are different types of of finance options available for businesses, such as: chattel mortgage, lease, and equipment finance.

Private sales

A private sale occurs when a buyer purchases a car from a private seller, rather than through a dealership. The car finance options can differ and may be limited when purchasing a car privately, however finance may also be obtained through a personal loan.

Types of car loans

Secured

A secured car loan means the car is being used as collateral. As the vehicle is used as security against the car loan, the lender can repossess ownership of the vehicle in the instance a borrower defaults on their loan. It is because of this security a secured car loan generally attracts a lower interest rate.

Unsecured

An unsecured car loan is a type of car loan that has no collateral. As an unsecured car loan does not take the vehicle as security, there is a higher risk involved for the lender if the borrower defaults on their loan. It is because of this higher risk unsecured car loans generally attract a higher interest rate.

Variable

A variable interest rate means your rate can increase and decrease during the duration of your loan, which can also impact your repayment. Rate fluctuations depend on both the lender and market changes.

Fixed

A fixed interest rate means your interest rate is fixed and will remain untouched throughout your car loan term.

Novated lease

A novated lease is available for business use where the employer pays to finance the car purchase. The employer will take the money from your pre-tax salary to make payments for the vehicle.

Chattel mortgage

A chattel mortgage is predominantly used for business purposes. The business has ownership over the vehicle but the lender has a ‘mortgage’ over it until the loan is paid.

How do I get a car loan?

There are plenty of options for you to obtain a car loan in Australia. You could seek to obtain car finance through your bank or an online lender. Alternatively, a broker can also help you obtain car finance.

Car brokers can do all of the work for you, from finding the car you’re looking for to organising the best car loan rate. They can do all of the communication with the seller, the negotiating of the price, and they can assist in organising the warranty and insurance coverage. Car brokers are the middle man who can reduce the stress and the hassle of buying a car.

Eligibility criteria for a car loan?

To be eligible for a car loan, you need to provide the lender with certain documents. These documents are:

Personal Identification

You will need to provide legal documentation with information such as your full name, age, birth date, citizenship information. This document can be your passport, driver’s license or state issued proof of ID card.

Proof of income

You will need to provide your 2 most recent payslips, and 3 months bank statements to indicate your income and outgoing expenditures.

Assets and liabilities

Proof of your assets and liabilities are also required to show your financial position. This should include any loans you currently have (such as mortgage, personal or credit card), superannuation, your share portfolio, and any properties or vehicles you own.

Car make, model and insurance

The lender will ask for details of the car you are planning to buy, including the make, model, year and price. Some lenders may also require auto insurance for the protection of the vehicle during the loan term.

Can credit history affect car loan rates?

A good credit score has many advantages and it can influence lenders to be more willing to accept your loan application. Depending on the lender, you may also be able to obtain a lower interest rate due to a high credit rating. You can check out your score from credit report agencies in Australia such as Experian, illion, or Equifax. Even with a low credit score, some lenders like carloans.com.au can help you get approved for a great car loan.

How do I apply for a car loan?

Once you have your documents ready and have chosen a car to purchase, you can easily apply online for a loan through lenders such as loans.com.au. Just fill out the online application, and a lender will contact you from there to assess your application and if approved, settle on your behalf.

Car loan approval process

Here are the general steps involved in applying for car finance:

Ready all of your documents:

Personal identification, proof of income, asset and liabilities, car details, and car insurance.

Apply online:

Complete and submit your application to your preferred lender.

Application reviewed:

Credit officers will assess your application if you're eligible for a car loan.

Loan funded:

Once you’ve been approval, you can receive your funds to buy your car. If you go with a car broker, you simply have to pick up your car.

Types of car loan lenders

There are different types of lenders that can provide auto loan financing, the two popular options are through lenders and car brokers.

Lenders

Lenders include the likes of the Big 4, as well as other smaller lenders. If you choose this route, you have the ability to choose your lender, loan and term. You’ll also be the one handling your application, from applying for a loan to picking up your car.

Car Broker

A car broker is a middleman who will be handling the entirety of your loan application, from finding a car for you, all the way through to settlement. All you need to do is pick up your car once everything is finalised. They often charge a fee for this service, however using a car broker can be beneficial in the long run as it can save you a lot of time during the car buying process. The car broker will also negotiate the purchase price of the car from the seller and seek the best interest rate on a car loan for you, which can end up saving you a lot of money overall.

What do you need to look for in a car loan?

Car loans do not all have the same structure - it will differ between lenders and depend on the type of car loan you are going to get. Here are the things you need to consider when looking for a car loan:

Annual fees and establishment fees

Some lenders will charge fees annually or for establishing the loan.

Free extra repayments

A feature that can let you make extra repayments without paying fees, so you can pay out the loan early.

Balloon payment

This feature lets you pay a lump sum at the end of your term, which generally means you will have a lower monthly loan repayment during your loan term. The amount of the lump sum is generally set at a percentage of the loan.

Variable or fixed rate

You will need to decide if you would like to opt for a variable rate, where the rate can fluctuate up or down during the loan term, or a fixed rate, where the interest rate will remain the same for the life of the loan. While fixed rate loans offer peace of mind that your repayments will remain the same for the entire loan term, a variable rate loan may be more attractive to you if you would like flexible features.

Loan term

The loan term you choose will have an impact on your repayments. A shorter one means higher repayments but a lower overall cost, as you will be paying interest for a shorter time period. A longer term means lower repayments but a higher overall cost, as you will be paying interest on your loan for a longer time period.

Scenarios

Here let’s see different scenarios. As an example, you are purchasing a new car.

Car: Subaru Outback ($50,000)

Interest rate: 3.29%

Loan amount: 40,000

Loan term: 5 years

1st scenario: What will my repayments be if I pay off weekly instead of monthly?

Weekly: $180.98 weekly

Fortnightly: $361.96 f/nightly

Monthly: $723.91 monthly

2nd scenario: What will my repayment be if I take out the loan with a 30% balloon vs no balloon

With 30% balloon: $493.57 monthly

No Balloon: $723.91 monthly

3rd scenario: What is the difference between buying a Subaru Outback ($50,000) with a rate of 7% with no annual fee, vs 6% with an annual fee of $100. Take note, we’ve added monthly payment and the fees, resulting in the total loan amount.

|

|

Monthly payment |

Fees |

Total loan amount |

|

7% interest rate no annual fee |

$792.05 monthly |

$0 |

$47,523 |

|

6% interest rate with $100 annual fee: |

$773.31 monthly |

$100 x 5 (years)= $500 |

$46,898.6 |

You can use our car loan calculator to explore what your repayments will be based on the specific information you input.

Additional Costs

Apart from the auto loan, there are other additional costs to consider when buying car. The most common costs are:

Stamp duty

This is a tax you need to pay when buying a car and it will vary from state to state where you purchased your vehicle. You can use a stamp duty calculator to know how much you need to pay.

Motor vehicle registration

You will need to register your vehicle, and this also comes at a price. If you are buying a used car you will need to pay to transfer the ownership. This transfer fee will vary in each state, ranging between $20 to $30.

Car insurance

You will need to protect your car from any unfortunate events. Comprehensive insurance or Compulsory Third Party Insurance (CTP) can give you the coverage you need.

Petrol

This will depend on how much you use your vehicle as well as the type of vehicle you have, but according to ASIC, the average Australian spends about $1,737 annually on fuel.

Regular servicing and repairs

You will need to set aside money for regular servicing and repairs. Experts recommend getting your car serviced every 15,000km or every 12 months - whichever comes first. There are websites available that can tell you the operation costs for your specific car model.

Road tolls

Toll charges will vary by toll road and type of vehicle. To find how much you will be charged, you can check your states toll charges.

Questions to ask a car loan broker or lender

Here are some questions to ask when getting auto loan financing, whether you’re getting it from a car loan broker or lender:

Accessing and monitoring your loan application online, as well as having multiple payment channels is very handy nowadays. Ask your lender about this.

Knowing how much you can borrow can help you set out your car-buying budget.

The length of your car loan application will vary since every lender is different. This can also help you plan ahead.

Disclaimer

**Rates as at 7 August 2023 for home owners. The interest rate is determined with reference to the age of the vehicle, eligibility criteria and the credit assessment, including home ownership. Interest rate loading may be applied. Vehicle age must be 12 years or less upon commencement of loan term. Balloon option available for fixed rate loan terms <5 years for vehicle age 4 years or less upon commencement of loan term. Target Market Determinations for this product available.

*The comparison rate is based on a $30,000 loan over 5 years. Warning: this comparison rate is true only for this example and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. Lending criteria, fees and conditions apply. Rates, fees and conditions are indicative, available for new loans only and subject to change without notice.

^For purchase of New / Demo vehicles defined as up to 12 months old with under 5000kms.

~Subject to provision of all required information and supporting documents on application.

+Loan terms over 5 years will incur 0.50% interest rate loading for fixed rate loan.

#Based on the dollar value in the search field with P&I repayments over the selected term, not including monthly fee, with balloon payment if entered.

Powered by:

![]() Savings.com.au

Savings.com.au

Savings.com.au Pty Ltd ACN 161 358 363 | Australian Financial Services Licence and Australian Credit Licence 515843